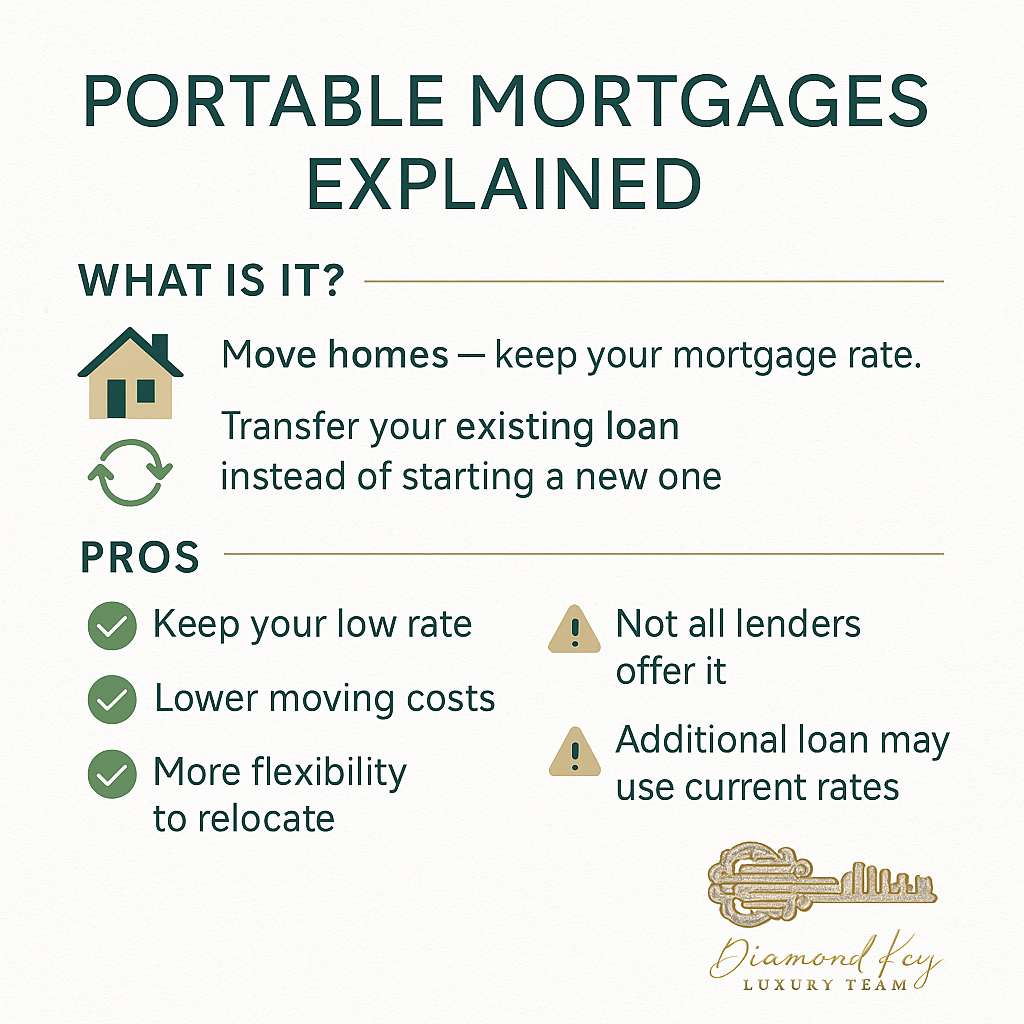

A portable mortgage is a home loan structure that — instead of being tied to a single home forever — would allow a homeowner to transfer their existing mortgage (interest rate, remaining balance, and loan terms) to a new home when they move. In effect, you “take your loan with you.” Under current U.S. norms, when you sell a house you pay off the mortgage and get a new one — but with a portable loan, you’d carry over your existing loan under its original terms.

The idea has gained renewed attention because many U.S. homeowners locked in historically low mortgage rates — say 3–4% in prior years — are now “stuck.” Moving often means giving up that low rate for a new loan at today’s 6%+ levels, so many stay put instead of upgrading, downsizing or relocating.

As of late 2025, the Federal Housing Finance Agency (FHFA) has publicly said it is “actively evaluating” making portable mortgages available in the United States.

Potential Benefits — Why This Could Matter for Homeowners

- Keep your low interest rate: If you locked in a favorable rate years ago, portability means you don’t lose that advantage just because you move.

- Avoid some of the costs of refinancing/new loan origination: Instead of applying for a brand-new mortgage — with lender fees, appraisal costs, underwriting, etc. — you simply transfer your existing loan.

- Reduce the “lock-in” effect: Many homeowners sit tight because giving up a low mortgage rate is too painful. If portability becomes available, it could prompt more moves, freeing up housing inventory and letting people more easily adjust home size/location based on life changes.

- More flexibility and mobility: For sellers who want to move — upsize, downsize, relocate for work or family — portability could remove a major financial barrier.

Downsides & What to Watch Out For

- Not all mortgages — or lenders — will offer porting: In many cases, “portable” loans simply aren’t on the table under U.S. mortgage-securitization norms.

- May still require additional borrowing (“blend and extend”): If your new home is more expensive than your current one, you’ll likely need to borrow extra at today’s (higher) rates — which could negate some benefits.

- Underwriting and eligibility still apply: Even though you’re porting an existing loan, lenders will reassess your finances and the new property, which means you might be rejected if circumstances changed (income, credit, etc.).

- Could raise rates generally: Because transferring mortgages across properties complicates the way loans are bundled and sold to investors, some experts warn that portable mortgages might lead to higher interest rates overall — which might end up hurting future buyers.

- Won’t help renters or buyers without a mortgage: Portable mortgage only benefits existing homeowners with an existing loan — first-time buyers or renters get no benefit, and affordability issues (high home prices, down payments) remain unchanged.

Bottom Line

A portable mortgage — if implemented — could be a powerful tool for homeowners sitting on low-rate loans who want more flexibility to move, upgrade, downsize, or simply change homes without suffering payment shock. For many long-term homeowners, it could unlock movement and free up housing inventory stuck because of the rate-lock-in effect.

But it’s not a panacea for wider housing-market problems: implementation complexity, limited availability, blended borrowing, and investor-market complications create real barriers. And for renters or buyers who don’t already own a home — this doesn’t improve affordability or access.

If you own a home with a favorable rate, keep an eye on FHFA developments — this could change how you think about your next move.

Thinking about making a move? Let’s talk strategy–click here to book a call.